Other Pages

- Opinion Poll

- About Us

- Send Your Story

- Contact Us

- Newsletter

- Privacy Policy

- Terms and Conditions

Lending and borrowing money for business is as old as business itself. But it is inherently problematic. As man continues to advance in business technology, it is expected that taking loans and repossessing such loans from defaulters will become easier and a lot less problematic than Shylock's business in Shakespeare's Merchant of Venice. Has it? In this piece, Ridwan Yusuf, for eight weeks, investigated the loan repossession techniques of Nigerian microlenders and finds disturbing truths.

Innocent of any criminal offence and not under arrest, nursing mother Akorede Abigael was imprisoned in a fetid toilet for five hours. Gnashing her teeth in frustration and moaning, Abigael clinged to her baby with one hand, and used the other to cover her nose.

Her offence? She defaulted on a short-term loan repayment.

Abigael is just one among thousands of Nigerians dying slowly and silently owing to ‘loan wolves’ of Nigeria who use uncanny and inhumane methods to retrieve loans given out.

Abigael had obtained a loan from Victory Microfinance Bank Abule Egba in Lagos. She had appeared with her group ‘Excel’ with incomplete funds and attempted to explain the circumstances surrounding her inability to pay. The lender didn’t listen. She must be humiliated along with her innocent baby.

“It was some years ago. What happened was that I was expecting some money but didn’t get it before my group’s meeting time,” she narrated. “In my group, ‘Excel’, we repay the loan every week. Unfortunately, my money was incomplete. I explained to their Business Manager, but he insisted his staff lock me up.”

Many patrons of microlenders in southwest Nigeria are familiar with the Yoruba phrase “Gb’omu le’ lanta”. It is a figure of speech alluding to the discomfort that comes with taking microloans from unforgiving lenders -- Microfinance Banks (MfBs) and Micro-finance Institutions (MFIs). It literally means to ‘place the breasts on a lit lantern’.

Numerous petty traders who take the loans stay till very late in the night in the market, using the lantern as a source of light so that they can sell enough to repay the loans along with interest before the due date. Yet, these borrowers — mostly unlettered petty traders and local artisans — still end up humiliated like Abigael, for failing to pay on time no thanks to poor sales.

Akorede Abigael

MFBs are easily accessible, thus, many small business owners in states like Lagos, Ekiti, Oyo, Osun, Ogun and Kwara; and other major Nigerian towns plus Abuja, run their business through small loans received. But while a few are able to manage the loans well and are guaranteed trouble-free transactions with the banks, a lot of borrowers usually have it tough repaying.

N20, 000, N50, 000, N60, 000, and more are loaned to interested persons, but the recovery methods are crude. If defaulters are not locked up in toilets, they are forcefully paraded in public to beg for alms or their obituaries are pasted, despite them being among the living. Fatimo Adeosun is an eyewitness of such molestation-disguised-as-loan-repossession at one of the offices of Asha Microfinance Bank in Ogun State. She says the molestation exists up to now.

“The woman defaulted for about four weeks, so they put cardboard around her neck with ‘debtor’ boldly written on it,” Adeosun recounts. “They then forced her to beg for money in the market.”

Abeeb Lawal works as a Credit Officer (CO) with a top Microfinance Bank in Lagos. He deals directly with borrowers of micro-credit loans and helps his employer recover loans obtained. When asked about predatory lenders with regard to small loans to traders, he disapproved of the recovery methods.

Lawal acknowledged that every money lender finds every possible means to get their money back, since some customers are not willing to service their loans. But he also holds that it is unacceptable and unlawful to lock defaulters up inside a toilet, humiliate or detain them. He believes court orders or police intervention should be enough. The loan officer reveals his bank's alternative.

“Every loan is risky, that is normal. So, we have to mitigate it through collaterals and guarantors. We put more emphasis on collateral and guarantor," Lawal explains. "When a client defaults, the next thing we do is we contact the guarantor. So the guarantor will have to put the client under pressure. Then, we usually involve a third party to the loan too. That is, the husband in case the wife is getting the loan, or the wife, if it is the husband who is getting the loan."

Contacting guarantors is usually enough most times to retrieve the loans for many of Lawal's clients. But in circumstances where the method is not effective, the lender turns it up a bit, without dehumanising his clients.

"We trigger the option of collateral. You know someone would not want to lose his or her valuable property," he says. “For small borrowers, we use their household goods as collateral, while we use hard collateral like cars, land, investments, etc for those who get support from us in millions of naira.”

Abeeb explained that for micro-loans given to small businesses, the bank he works for “snaps the collateral with the client”. This he says, will serve as a proof in case of any brouhaha in the future. It could be a television, refrigerator, electric generator or other appliances the loanee owns.

In this youth-dominated digital age, micro-credit loans via the internet, and in the comfort of one’s room have towered above brick and mortar MFBs’ and MFIs’. Credit is now boundless because of technology and innovation. But retrieval is no less messy for defaulters. They are increasingly dependent on the use of personal data such as phone contacts and social relationships.

In this case, borrowers are assured of stressless loan acquisition, but they are never informed that the consequence of defaulting, even due to no fault of theirs, is public announcement. Every contact in the borrower's phone book and social networks is notified -- a daring attempt to shame clients to pay.

Tales of embarrassment lace the experiences of citizens as they struggle to secure funds to survive in a tough country like Nigeria. Across the federation, app-based lenders have a poor reputation of managing loan retrieval. This among other factors prompted the National Information Technology Development Agency (NITDA) to use a financial technology (fintech) company as a scapegoat recently. NITDA wielded its hammer on Sokoloan Lending in August. Sokoloan, a Chinese company based in Lagos Nigeria was fined N10 million for invasion of customers’ privacy.

Although NITDA came up with the Nigeria Data Protection Regulations (NDPR) in 2019, which specifically addresses Data Privacy and Protection in the country, there is no specific statute regulating data privacy and protection.

Sokoloan app

Sokoloan App -- hosted on Google Play Store and without any brick and mortar structure to its name -- grants its customers uncollateralized loans and requires them to download its mobile application on their phone. Having Sokoloan App on one’s phone and getting loan approved (usually within a short period) means the fintech company has access to all the contacts on the Subscriber Identification Module (SIM) card of a loanee -- a controversial arrangement. With that, people’s information is being wrongly used by the lender, exposing loanees and their associates to abuse.

Eric Afam Ozegbe, an Information Technology (IT) Support Specialist, recounted how his wife, Assumpta Ozegbe was embarrassed and even labeled “a suspected criminal and fraudster” by Sokoloan. The ‘company’ sent a message to Afam Ozegbe’s business partners’ phone number saved on his wife’s SIM card.

The message reads: This is to inform the general public that ASSUMPTA OZEGBE 090353***** is a Suspected Criminal n Fraudster on the run with company money. Call and inform family.

Ozegbe finds it disgusting.

“In April, my wife took a loan of N2,500 from Sokoloan. She was supposed to pay back in seven days, but couldn’t -- due to the Bank Verification Number (BVN) challenge. The BVN issue is related to discrepancies in her age,” he explained. “With my line, I called the number they used to send their message, the person insulted my generation, and even tried to hack my WhatsApp number. I had two-step authentication, so they could not hack my WhatsApp.”

Ozegbe found a way to swiftly refund the loan which had at the time come to N9,870 plus interest.

“Sokoloan is sending Nigerians to an early grave with their blackmail, I tell you,” he rued.

At another time, Ozegbe received another message from Sokoloan about one Mrs Naomi Bassey Opeh who defaulted. “I don’t even know this person,” Ozegbe grumbled.

A screenshot of the message Ozegbe received from Sokoloan

In August, new father Tosin Awojide defaulted for only one day. He was humiliated by Sokoloan.

“They already sent messages with my pictures on WhatsApp to my contacts. It is still shaking me till now as I am typing. I opted for the loan because I needed to clear up the hospital bill for my newborn who had issues three days after his birth,” Awojide said.

Contacting Sokoloan via email with borrowers' complaints about the humiliation suffered at their hands, the company dodged the inquiry. Rather, the company requested for “the content of such a message and the phone number linked to it”.

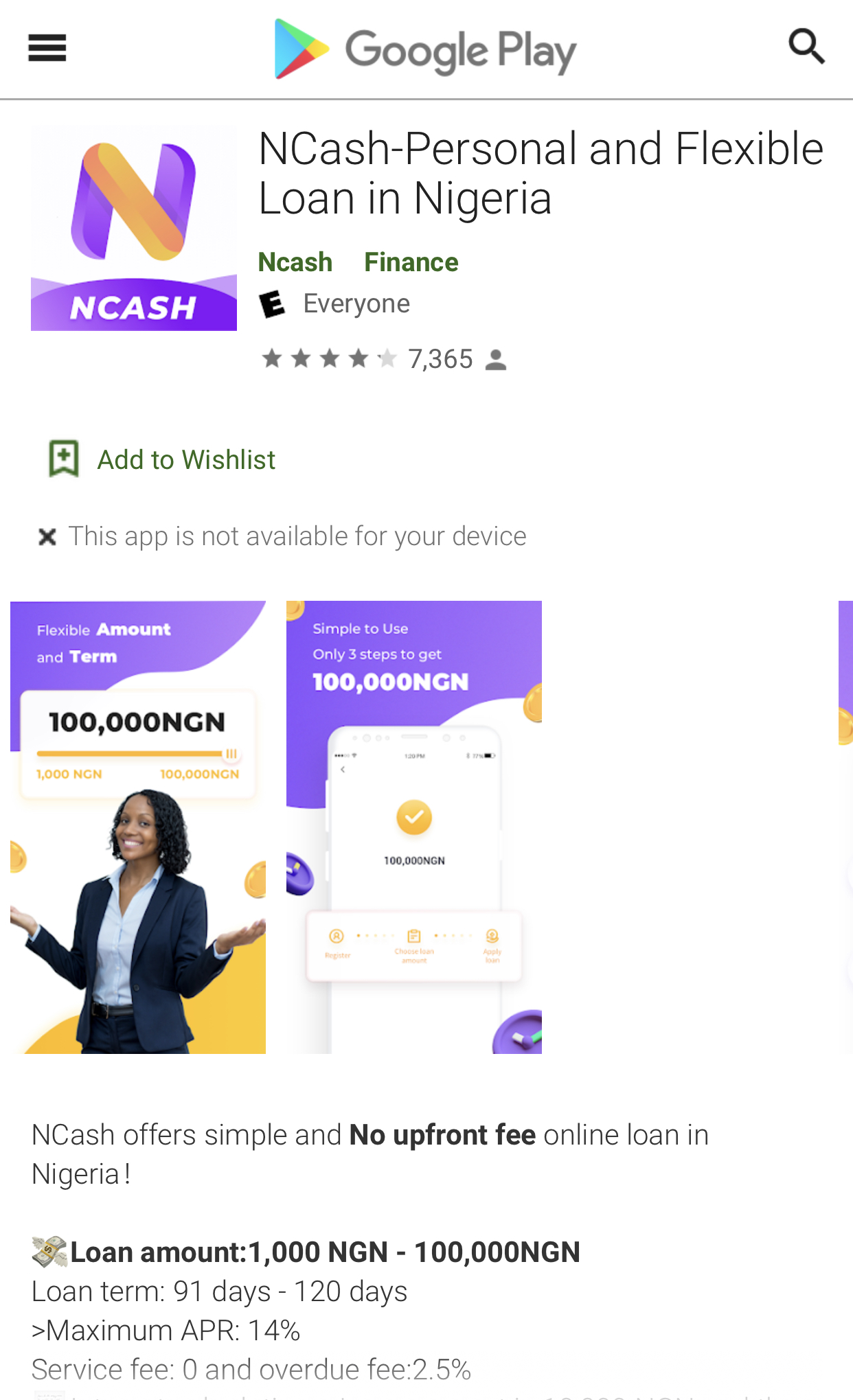

Akin to Sokoloan, fintech creditors like N-CASH usually ask for permission to access the contacts on the SIM card before a loan is approved. Without properly vetting loan applicants' identities, they resort to publicly shaming the defaulter and ‘disturbing’ everyone in a person’s inner circle by sending WhatsApp and text messages to them.

On 17 August, N-CASH sent a text message to Olu Samuel’s wife -- apparently after the borrower was unable to pay back on the due date. In the message, the debtor was referred to as “deceitful” and “chronic debtor” who “is on the run”. Weirdly, Samuel’s wife, who knows nothing about the loan, was threatened.

NCash app

Efforts were made to get NCash’s reaction. However, emails sent to the platform’s known email address bounced more than once.

Many Nigerians have demanded that what they now describe as ‘loan sharks’ must exit the tech space.

This reporter sighted a WhatsApp chat between a ‘remorseful’ defaulter and a Lagos-based borrower, AjeLoan.

AjeLoan's website

In a dehumanising tone, AjeLoan, conversing via a phone number Truecaller application identifies as ‘Iya Hannah’, destroyed the debtor. “You are an animal; you want to ruin your future, right? You sit there and dictate for me when you want to make payment,” she flared up.

When the customer replied with apologies, explanation and a promise to make the payment as soon as the money was ready, Iya Hannah followed with more fire. She issued threat of monumental humiliation, one which AjeLoan accepts could cause the defaulter to commit suicide.

“The kind of embarrassment that will hit you now, you won’t be able to stand it. You might even end up committing suicide.”

AjeLoan humiliating a customer

This reporter reached out to ‘Iya Hannah’, and put his discovery to her.

“Lol," she responded. "Maybe you should go back to the person that sent you here. Everything I ought to do regarding this case, I dropped it. So all of this is going nowhere. I wonder where you all were when this young [sic] took the loan and refused to pay back, and then you come telling me I threatened her to suicide. Haba.”

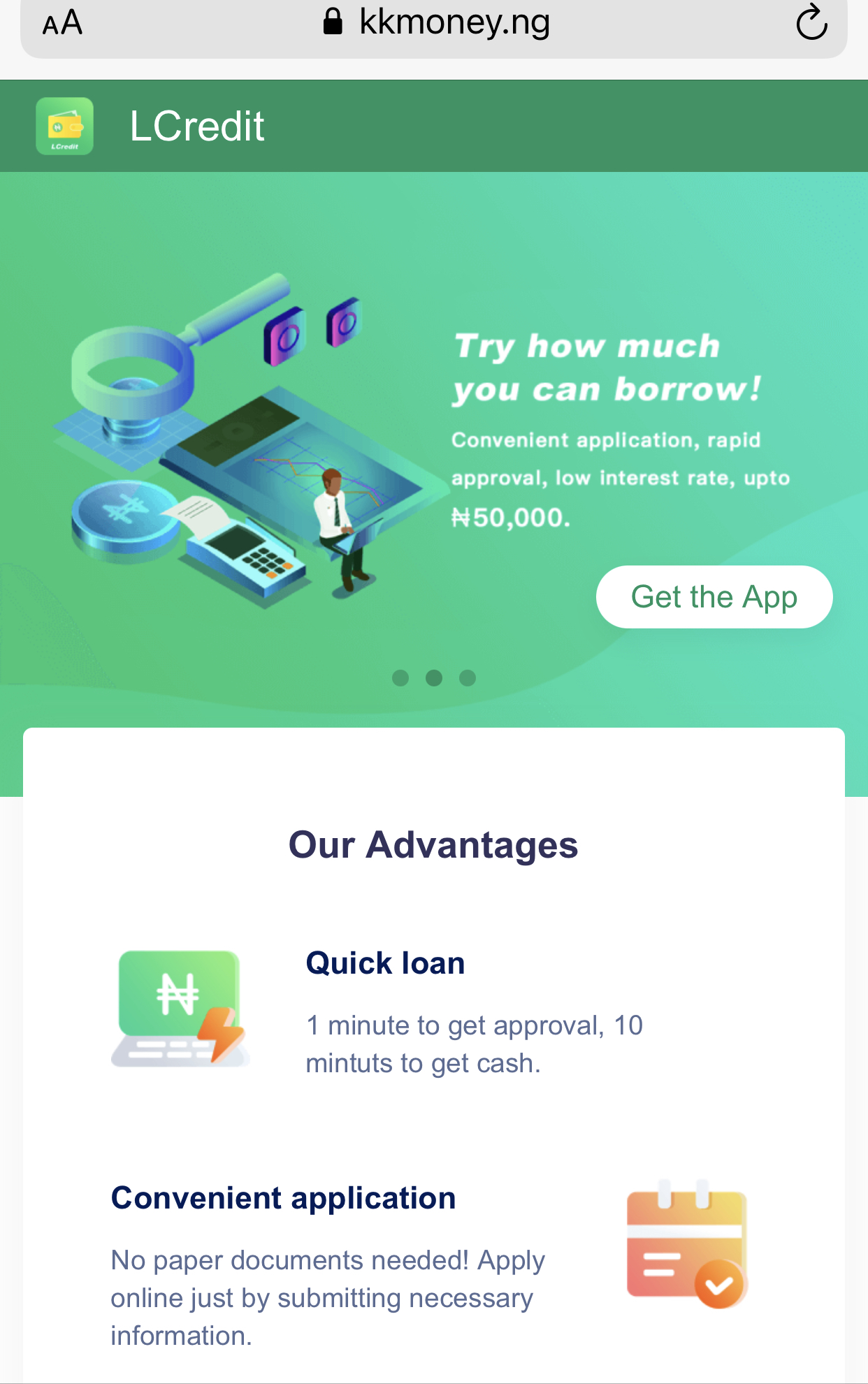

LCredit's site

Owing to their trademark threat, Chinwe Sandra [not real name] had to plead with loan company, LCredit not to get in touch with anyone on her contact list.

Sandra's message to LCredit

She had defaulted by paying two days late because the little she earns was not able to offset the loans. Within those two days, two of her contacts called to inform her of their unpleasant experience at the hands of LCredit.

“I cannot wait to finish repaying them and uninstall their application from my phone. Their issue gives me sleepless nights,” Sandra laments.

LCredit didn't respond to all efforts to get their side of the story.

Dike Philip Chijioke, Special Assistant on Media to Ugonna Ozurigbo, a member of the House of Representatives (Nigeria), described the current crop of online loan apps as “really crazy”.

According to him, fintech creditor, Creditmesan, involved him in “a loan that isn't my concern”. The message below:

Quite oddly, Creditmesan has no traceable contact on cyberspace.

Privacy concerns

What rights do online lending platforms have to share accessed users’ contact list with third parties because they defaulted?

This reporter reviewed the terms of service of the loan apps mentioned in this piece -- Sokoloan, NCash, AjeLoan, and LCredit. All four failed to disclose to users downloading the apps that their rights of access to users’ contact lists would be shared with third parties if they defaulted. This does not conform with policies of Google Play Store, the platform hosting the apps.

The updated data privacy policy on the Google Play Store stipulates that apps that offer financial services on its platform should disclose to users what it intends to use their personal information for.

“Your app must post a privacy policy that, together with any in-app disclosures, explain what user data your app collects and transmits, how it’s used, and the type of parties with whom it’s shared,” the policy reads.

Expert speaks

Question exists over whether most Nigerian-based loan apps are appropriately registered on the Corporate Affairs Commission (CAC’s) database. CAC is the body responsible for the regulation and management of companies in Nigeria. But a Business Development Advisor, Stanley Omonode (not real name), who consults for two Nigerian-based loan apps, beamed his expert light on the subject. He explained that there is essentially no loan app that is not properly registered with the CAC. According to him, many of them opt to use their trade name/brand name vis-à-vis their apps. Several companies, in some cases co-owned by foreigners, might even have multiple loan apps and use different names.

“These loan apps work alongside BVN, whose doorway cannot be opened to just anybody,” Omonode said. “The BVN porch also accesses the credit bureau — to know how loan worthy an individual is. I expect they’d have a record with the Nigeria Inter-Bank Settlement System Plc (NIBSS) too.

“Had it been they were not properly registered, they’d have been flagged by authorities.”

CBN's stance

In August, the Central Bank of Nigeria (CBN) secured a court injunction to freeze the bank accounts of at least four fintech firms ‘for operating as asset management companies without licence’. Via mail, I asked the CBN what their rules say about the operation of online loan apps who don’t have a physical office, but offer solely short term loans to Nigerians. The apex bank is yet to respond.

Meanwhile, a relevant CBN reaction, from 2019 may suffice as the bank's official stand on the matter. Per Tribune, Isaac Okorafor, then Director of Corporate Communications of the CBN said the contract between a lender (banks or online credit advancement firms) and its customer did not involve the regulator but the parties concerned. Okorafor added that each of them had rights to sue and be sued and so any party that is treated unlawfully can go to court.

“The law guiding loan repayment specifies that the borrower must ascertain whether the repayment schedule proposed by the bank is convenient to it and its line of business. We are neither a human rights body nor the police. The contractual relationship between a customer and his bank is exclusive of CBN’s role, therefore, any debtor who feels his or her rights have been violated can seek redress in the law courts,” he explained.

It is understood that CBN has repeatedly warned the general public against patronising unlicensed and illegal financial institutions. Reason being that such institutions could equally use unlawful means to recover their money. All CBN-licensed lenders are guided by the Banks and Other Financial Institutions Act as amended), available in public domain.

2 Comment(s)